Published in South Florida Hospital and Healthcare Association Newsline –

So here we are, seven or eight months into this thing, and we still haven’t quite figured it out. We know it’s deadly, we know it affects certain among us disproportionately, and, unfortunately, we know it’s not going to fade away anytime soon. We can see and feel some of the effects in our everyday lives—the heroism of our essential workers, the economic turmoil around us, the isolation of “social distancing,” and the tragedy of lives lost too soon.

We know we’ll get through this, but not without some fundamental changes and impacts to our healthcare system. And it’s not just the provider sector of the industry that is struggling to adapt to the new normal and trying to anticipate what “recovery” looks like. The entire industry is undergoing fundamental change. As we look at the big picture, let’s see if we can understand some of the effects the pandemic has had so far, which might help us figure out where things might go from here.

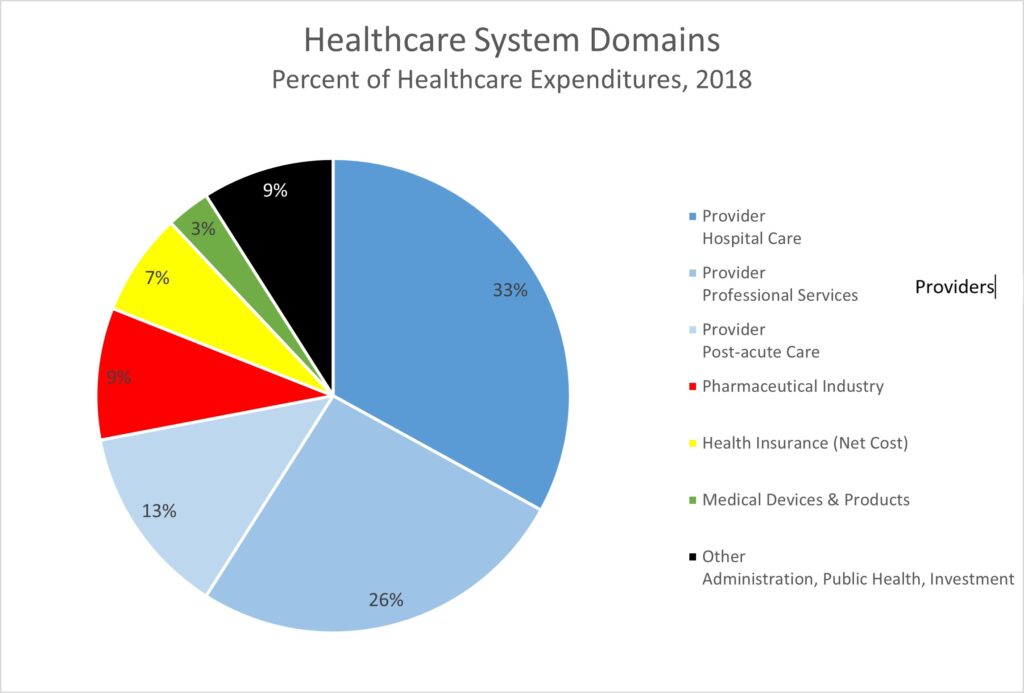

Rather simplistically, we can define our healthcare system as having four major domains,1 all of which have had some degree of impact due to the COVID-19 pandemic. By far, the largest domain is the healthcare delivery or provider domain, and this is also the domain that tends to drive the operations of the other major industry sectors. Here is the breakdown by domain.

| Healthcare Sector | % of Healthcare Expenditures |

|---|---|

|

Providers: Hospital care, physician care, long-term care, etc.

|

62% |

|

Pharmaceutical Industry

|

9% |

|

Medical Insurance/Managed Care (Net Cost) |

7% |

|

Manufacturers of Medical Devices and Products |

3% |

|

Other/Miscellaneous |

9% |

Providers:

Providers have had the toughest time during the pandemic, and the effect on their operations has been well documented. For hospitals, the increase in COVID cases, requiring a greater intensity of labor, care, and services than the typical patient—along with a concomitant decrease in routine care and elective cases as well as emergency room visits—has endangered the financial picture and even the solvency of many institutions, particularly those that treat safety net populations. Likewise, physicians have seen huge drops in patient visits, and even the unprecedented spike in telehealth visits has not been enough to keep some practices viable. In fact, after the precipitous drop in physician visits early in the pandemic, the level of physician visits continues to be about 10% below pre-COVID levels and the cumulative number of lost visits continues to grow.2

Post-acute care institutions, with their frail and elderly populations, have been hit especially hard; not only have they had significant staffing issues, but some have had to limit capacity by converting semi-private rooms to private ones to inhibit the spread of infection. And the overall demand for their services has been lower due to fewer hospital surgery patients entering skilled nursing facilities, a general fear of placing a loved one in a long-term care facility, and more family caregivers having time at home to care for loved ones. Home care organizations have had a hodgepodge of effects: looser CMS regulations have allowed initiation of care to occur via telehealth, and the higher acuity of patients seen in home care settings (versus in institutional settings) has generally led to higher reimbursements. However, fear of virus spread has led to several staffing-related issues—less staff being able or willing to go into patients’ homes, fewer patients wanting to allow home health therapists and aides into their private dwellings, inadequate PPE and infection control training for home care workers, and contract staff working for multiple agencies being unwitting COVID-19 hosts.

Pharmaceutical Industry:

The impact of COVID-19 on the pharmaceutical industry has been substantial but not devastating. If anything, the pandemic has highlighted the significance of Big Pharma and its role in developing vaccines and treatments for those affected by COVID and other diseases. Most major pharmaceutical manufacturers—Merck, Eli Lilly, Moderna, Johnson & Johnson, and others—have revised their earnings estimates downwards to reflect the decline in sales due to lower provider visits and treatments. However, even their Q2 earnings forecasts, despite revenue downturns, anticipate healthy bottom line profits.3 Perhaps not surprising, COVID has led to much higher utilization of mail-order pharmacies and an enhanced role for pharmacy benefit managers to ensure continued access to necessary drugs for patients, commercial pharmacies, and healthcare institutions.

The most significant COVID-related impact on the pharmaceutical industry, however, has not been the demand for needed medications but on the supply side of the equation. The global nature of COVID, its origin in China, and its disproportionate impact on India have led to severe disruptions in the pharmaceutical supply chain. Pharmaceutical raw materials, called active pharmaceutical ingredients or APIs, and generic medicines often come from China or India. In fact, up to 72% of APIs and generics are manufactured in foreign countries.4 Various trade restrictions and virus-related issues have slowed the supply chain and caused significant increases in the cost of raw materials, which have in turn caused shortages of emergency, anesthesia, and pain management drugs. This has led to a national resolve to produce more medications domestically, but that effort will take years to grow and flourish. Meanwhile, with the laser-focus on COVID drug development, clinical trials for non-COVID conditions are likely to be slower and more expensive. Although the short- to medium-term outlook for pharma is not as despairing as that for providers, there are significant warning signs, like the incessant pressure for lower drug prices, the slow pace of medication approval, and the difficult sourcing of raw materials, that that the industry will have to contend with.

Health Insurance Industry:

Early results show that the health insurance industry has done exceptionally well during the pandemic. Perhaps this is no surprise, considering that the percent of premium dollars that is dedicated to actual payment for medical care (known as the medical loss ratio) has taken a nosedive during the pandemic as beneficiaries have put off diagnostic tests, routine care, elective surgeries, and even ED visits. Humana, Cigna, United, Centene—many of the big players in health insurance—have had record-breaking financial results during the pandemic.5 However, even though claims payouts have been much lower during COVID and the resultant short-term gain has been substantial, the longer-term outlook is much more questionable. Since health plans are typically required to maintain a threshold medical loss ratio and must rebate employers and patients when they do not, the financial boon may be short-lived. In addition, Medicaid plans, which have seen a sharp increase in enrollment during the pandemic, will need to look out for state budget shortfalls portending cuts to Medicaid budgets. Even states considering Medicaid expansion have shelved those plans until the impact of COVID to state budgets is clearer.

Health plan executives know that, sooner or later, the chickens will come home to roost. The pent-up demand for services, the higher cost of treating those who have not adequately cared for their chronic conditions during the pandemic, and the number of employers (paying the bulk of the premiums) going out of business or slashing healthcare benefits to stay afloat, are all ominous warning signs that will affect industry performance and earnings down the road.

Medical Device Industry:

Like the pharmaceutical industry, the medical device and equipment industry depends heavily on regulatory approval for market entry and provider adoption for market growth. Similarly, many of the trends and indicators which affect the pharmaceutical industry also affect the medical device, equipment, and supply industry. The device industry has had to ramp up production of PPE, ventilators, and other COVID-related supplies and has therefore had some short-term revenue gains on those products. But the depressed demand for surgical devices, the lower availability of capital from providers to purchase supplies and equipment, the hyper-focus on COVID—leading to delayed non-COVID product releases and slowdowns in non-COVID clinical trials—and the ongoing international trade issues affecting import tariffs and export restrictions, will all harm the medical device industry.

Final thoughts:

With this mixed bag of results and effects of COVID-19, let’s get back to one of our original questions—where do we go from here? The answers are not entirely clear, but we can learn from what we have experienced so far.

- First of all, there are obviously transformative, irrevocable changes occurring in the healthcare industry at large which will last well beyond the pandemic itself.

- The delays in patient diagnosis, treatment, and recovery will inevitably lead to a surge in demand for healthcare services and an increase in the cost of care once members of the general public become more comfortable seeking necessary care from their providers. However, this demand may lead to an exacerbation of the looming scarcity of labor already seen in the provider workforce and more supply-side equipment and pharmaceutical shortages.

- Without a doubt, the digital revolution in healthcare is here. During the pandemic, providers and device manufacturers have had to develop digital solutions for patient access and patient engagement and telehealth technologies for patient treatment. COVID has hastened consumer adoption of digital technologies, greater interoperability among vendors and providers, and faster development times for digital product innovation.

- The shift from institutional care to non-institutional care will continue. With more and more care being delivered outside the walls of institutions, some of the investment in hospital innovation may convert to home-based, remote patient monitoring devices and technologies.

- During COVID, the speed of federal regulatory review, which has historically moved at a snail’s pace, has actually stepped up. Despite receiving some criticism for early COVID missteps and misinformation, the federal government deserves some credit for speeding up the regulatory approval process for new vaccines and treatments, providing financial incentives for businesses to develop critical PPE, and developing criteria to qualify for enhanced telehealth reimbursement. If government officials become convinced that they can actually improve care and save money by maintaining some of these processes during non-pandemic times, there should be positive rippling effects throughout the healthcare industry.

- Because of COVID’s lingering effects and a slower-than-anticipated economic recovery, there is some recognition among legislative and regulatory leaders that the provider segment of the industry may need further support. It is likely that some of the newer and untried value-based initiatives may slow down to stabilize the industry before the next wave of transformative change proposals.

- Although healthcare M&A activity may have slowed slightly during the pandemic, it will probably return with a vengeance. As the industry gets back on its feet and the dust begins to settle on which healthcare organizations have prospered, which have endured, and which have stumbled, there will be winners and losers, innovation champions and business failures. Larger organizations with stronger balance sheets and the ability to scale will acquire or force the market exit of their smaller, weaker, and less flexible counterparts.

Of course, these conjectures are only educated guesses based on what seems to have happened during the first several months of the pandemic. There are environmental factors, political considerations, and totally unanticipated events that could create new risks or opportunities or even change the trajectory for the healthcare industry. For any sector of the industry, however, the best bet to come out of this on the other side is to stay safe, to remain vigilant, to be nimble, to embrace innovation, and to stay focused on the health and wellbeing of its employees, its patients, its clients, and its external constituents.

- https://www.cms.gov/files/document/highlights.pdf, National Health Expenditures2018 Highlights

- https://www.commonwealthfund.org/publications/2020/aug/impact-covid-19-pandemic-outpatient-visits-changing-patterns-care-newest

- https://www.iqvia.com/library/white-papers/monitoring-the-impact-of-covid-19-on-the-pharmaceutical-market

- https://www.fticonsulting.com/insights/articles/covid-19-impact-global-pharmaceutical-medical-product-supply-chain

- https://www.healthcaredive.com/news/payers-saw-massive-q2-profits-as-covid-19-deferred-care/582993/